How to Find Pre-Foreclosure Leads in Florida (2026 Investor Guide)

How to Find Pre-Foreclosure Leads in Florida (2026 Investor Guide)

TL;DR: Florida ranks among the top states for pre-foreclosure investing because its judicial foreclosure process stretches 12 to 24 months from first filing to auction. That long window creates motivated sellers who need solutions fast. The leads come from lis pendens filings at county clerk offices, but the real advantage belongs to investors who stack multiple distress signals and reach homeowners before the competition. This guide covers where to find filings, which counties produce the most volume, and how to prioritize outreach.

Every real estate wholesaler in Florida pulls the same lis pendens list. The data is public. The county clerk portals are free. And 400 other investors are mailing the same names on the same Monday.

The difference between closing deals and burning marketing budget is not finding leads. It is finding the right leads at the right time, before everyone else finds them. Florida has structural advantages: a judicial process that takes months to years, an insurance crisis pushing homeowners into distress, and a massive non-owner-occupied property base whose sellers make financial, not emotional, decisions.

Florida's Judicial Foreclosure Process: The Basics

Florida is a judicial foreclosure state. Every foreclosure must pass through the court system before a property can be sold at auction. There is no non-judicial shortcut.

The process starts when a lender files a lis pendens (Latin for "suit pending") with the County Clerk of Courts. Under Florida Statute Chapter 702, the borrower has 20 days to respond after being served.

From that first filing, the timeline looks roughly like this:

- Lis pendens filed and borrower served (Day 0)

- Borrower response period (20 days)

- Discovery and mandatory mediation (varies by county, often 3 to 6 months)

- Summary judgment or trial (6 to 12 months after filing in uncontested cases)

- Final judgment entered (court sets sale date)

- Foreclosure sale/auction (typically 30+ days after judgment)

In practice, the full timeline from lis pendens to auction runs 12 to 24 months in uncontested cases. Contested filings in busy jurisdictions like Miami-Dade and Broward can stretch past three years. This extended timeline is the single biggest advantage for investors. The early window, the first 30 to 60 days after filing, is where the best deals happen.

Where Pre-Foreclosure Leads Come From in Florida

County Clerk of Courts (Primary Source)

Every lis pendens in Florida is recorded at the County Clerk of Courts. Most major counties offer online search portals. Miami-Dade and Broward update near-daily with decent data exports. Hillsborough and Orange have solid portals with weekly or near-daily updates. Smaller counties may update weekly; a few still require in-person requests.

Pulling raw data means logging into each portal, parsing inconsistent formats, cross-referencing with property records, then skip tracing. Covering three or more counties takes 10 to 15 hours per week.

Aggregated Data Platforms

Most investors use third-party platforms that index public records across counties. The tradeoff is freshness. Many platforms batch updates weekly or resell data that is already two to four weeks old. A seller at week three of a lis pendens filing has not yet been contacted by dozens of competitors. The same seller at month nine has heard every pitch. Freshness is the edge.

Which Florida Counties Produce the Most Pre-Foreclosure Leads

Volume concentrates in the state's largest metro areas. Here are the counties worth prioritizing and why.

Miami-Dade County

Population 2.7 million. Consistently the highest pre-foreclosure volume in Florida. Condo associations file aggressively, creating stacked signals. Zip codes in Hialeah, Homestead, and Opa-locka offer better entry pricing than the southeast corridor.

Broward County (Fort Lauderdale)

Second in population and pre-foreclosure activity. Pompano Beach, Lauderhill, and Miramar produce consistent filings. Entry prices are often lower than comparable Miami-Dade neighborhoods, with strong rental demand.

Palm Beach County

Higher price points (Boca Raton, Delray Beach, West Palm Beach) with a steady pre-foreclosure pipeline. Works well for luxury flips or buy-and-hold in the coastal corridor.

Hillsborough County (Tampa)

Price appreciation from 2020 through 2023 left some buyers overleveraged. Brandon, Riverview, and East Tampa have active wholesale markets.

Orange County (Orlando)

The short-term rental market near Disney and Universal corridors creates a buyer pool for distressed properties. Investor-owned properties in distress are common. Owners are often absent and making purely financial decisions.

Duval County (Jacksonville)

Less investor competition than South Florida, solid volume, and better conversion rates for wholesalers willing to work a less saturated market.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

Florida-Specific Factors That Drive Distress

The Insurance Crisis

Florida homeowners insurance premiums have more than doubled in many coastal areas since 2022. Multiple carriers have exited the state entirely. Citizens Property Insurance, the state's insurer of last resort, has absorbed hundreds of thousands of policies.

For pre-foreclosure investors, this matters because insurance costs are a hidden driver of distress that does not appear in lis pendens data. A homeowner with a manageable mortgage payment can be pushed into default by an annual insurance premium of $8,000 to $15,000 on a property that cost $3,000 to insure four years ago. South Florida and coastal corridor properties are most affected.

When evaluating leads in flood zones or coastal areas, always factor current insurance costs into the deal analysis.

Florida's Homestead Exemption

Florida's Constitution (Article X, Section 4) provides one of the strongest homestead exemptions in the country. A primary residence is protected from most creditor claims, with no cap on property value. The exemption does not protect against the mortgage lender or HOA enforcement. A seller with equity in a homesteaded property may be able to refinance or list at market value rather than accepting a discount.

HOA and Condo Association Liens

Florida grants HOAs and condo associations strong lien rights. Associations can foreclose for unpaid dues independently of the mortgage lender. In South Florida, properties with both an HOA lien and a mortgage lis pendens running simultaneously are common. That dual pressure is a strong motivation signal.

Non-Resident Property Owners

Florida has an unusually high share of non-resident owners. Absentee owners in distress are often easier to negotiate with because the decision is financial, not emotional. Filtering for non-owner-occupied plus distress signals typically produces the fastest negotiations.

The Execution Chain: Working Leads From Filing to Offer

1. Pull Fresh Filings Weekly

Set up a system to capture new lis pendens filings within 7 days of recording. Timing is the edge.

2. Pre-Qualify Before Skip Tracing

Skip tracing costs money. Do not trace every filing uniformly. Filter first:

- Filing date within the last 90 days (fresher leads are more receptive)

- Property value in a range that fits the buyer pool

- At least one additional distress signal stacked on the lis pendens

Trace the top 20 to 30 percent of filtered leads.

3. Segment and Sequence Outreach

Skip tracing results come with confidence scores. A cell phone match at 95 percent confidence is worth a call. A landline at 40 percent gets a postcard. For high-motivation leads (multiple signals, recent filing), run a sequence: postcard on day one, phone call on day seven, follow-up on day fourteen. Lower-motivation leads get one postcard and a 45-day follow-up.

4. Track Status Changes

Lis pendens cases evolve. Dismissals, new listings, and auction dates all change the urgency. A lead that was cold at month two may be urgent at month eleven. Build a CRM workflow that re-flags leads on status changes.

Why Single-Signal Lists Fail in Florida

The core problem with lis pendens data is that everyone has it. It is public, free, and every wholesaler who has been in the business longer than 60 days has mailed a lis pendens list. In Miami-Dade and Broward, the saturation is extreme.

The solution is lead prioritization by signal depth, not signal presence. Instead of "this property has a lis pendens," the question becomes:

- Does the property also have unpaid property taxes? (Stacked financial pressure)

- Is there an HOA lien on top of the lis pendens? (Multiple creditors)

- Was the property purchased in 2020 through 2022 at peak pricing? (Higher probability of negative equity)

- Is it non-owner-occupied? (Less emotional resistance to a sale)

- Has the owner shown prior tax delinquency? (Pattern of financial stress, not a one-time event)

- How recent is the filing? (30 days old versus 18 months old is a completely different conversation)

A property with three or four stacked distress indicators is dramatically more motivated than one with a lis pendens alone. The investors closing consistent deals in Florida are the ones who filter by signal depth, not the ones who mail the most postcards.

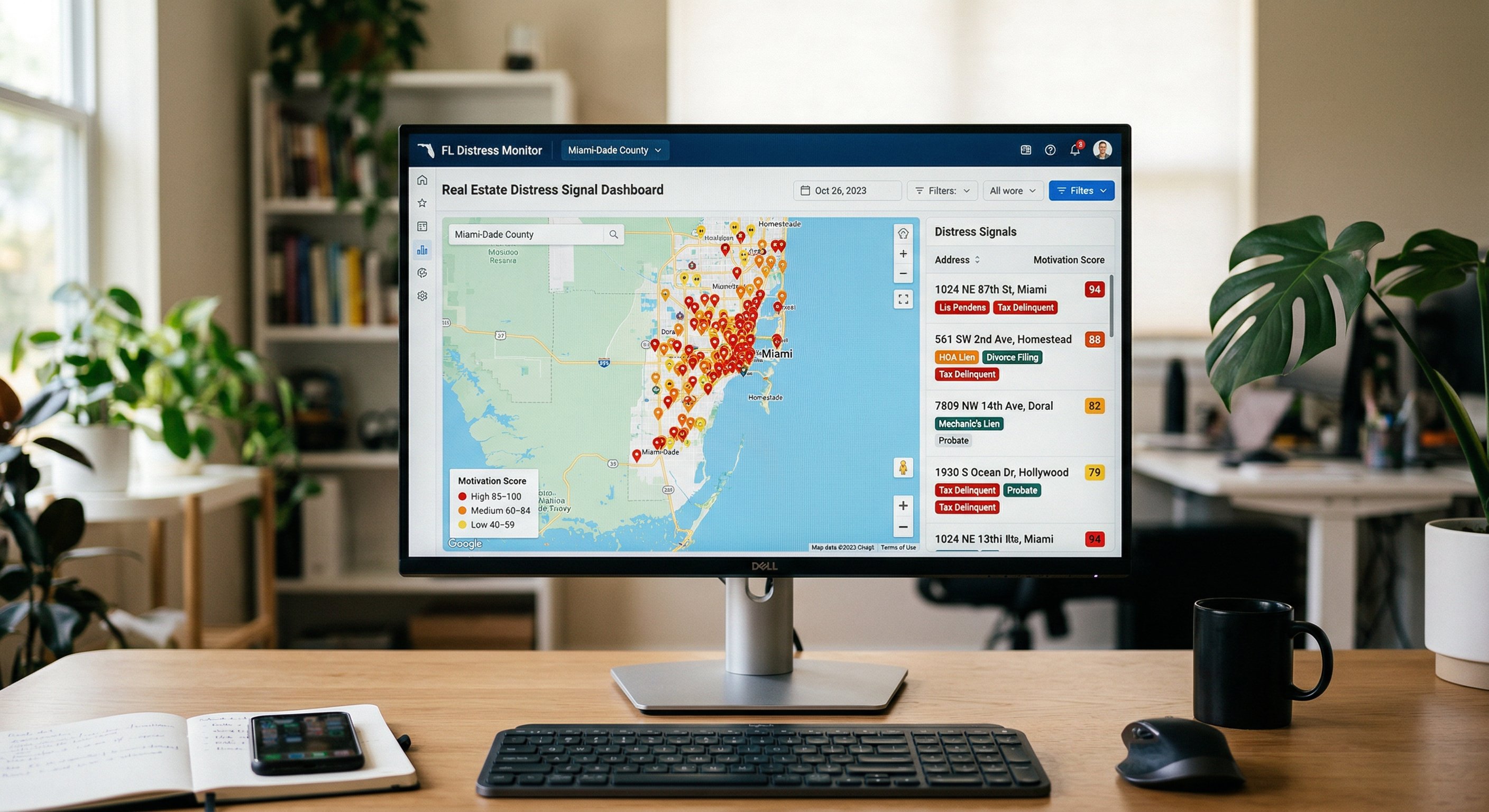

Browse every active pre-foreclosure in Florida's major counties, filtered by motivation score, signal count, and filing date, on DistressIQ.

Frequently Asked Questions

How does someone find pre-foreclosure leads in Florida for free?

Florida lis pendens filings are public records available through each county's Clerk of Courts. The limitation is that raw court records are unfiltered. To turn filings into actionable leads, cross-referencing with property records, tax data, and skip tracing is necessary. Platforms like DistressIQ aggregate this data across 90+ counties and allow browsing before paying for contact details.

How long does the pre-foreclosure process take in Florida?

Florida's judicial foreclosure process typically runs 12 to 24 months from the initial lis pendens filing to the foreclosure auction. The borrower has 20 days to respond to the complaint after being served. Counties with heavier court dockets, particularly in South Florida, often see timelines extend past two years in contested cases. This extended window benefits investors because sellers have time to negotiate without an immediate forced sale deadline. Under Florida Statute Chapter 702, the court must enter final judgment before scheduling a sale.

Which Florida counties have the most pre-foreclosure filings?

Miami-Dade, Broward, Palm Beach, Hillsborough (Tampa), and Orange (Orlando) consistently lead the state in pre-foreclosure volume. Miami-Dade produces the most filings due to its population size (2.7 million) and aggressive condo association lien practices. Duval County (Jacksonville) has meaningful volume with notably less investor competition, making it attractive for wholesalers willing to work a less saturated market. Volume generally tracks population density and housing stock size.

What role does Florida's insurance crisis play in pre-foreclosure activity?

Insurance premiums in coastal Florida have more than doubled since 2022. Annual premiums of $8,000 to $15,000 are now common for properties that cost $3,000 to insure four years ago. This cost pressure pushes overleveraged homeowners into default even when their mortgage payment is manageable. Insurance-driven distress is most visible in South Florida and coastal corridor properties. Checking current insurance costs is essential when evaluating leads in flood zones.

Is Florida's homestead exemption relevant to pre-foreclosure investing?

Yes. Florida's homestead exemption (Article X, Section 4 of the Florida Constitution) protects a primary residence from most creditor claims with no dollar cap. However, it does not protect against the mortgage lender or HOA enforcement. For investors, this means a homeowner with significant equity in a homesteaded property may be able to refinance or list at market value rather than accept a discounted offer. Always verify the equity position before investing substantial outreach effort on a lead.

What is the difference between a lis pendens and a notice of default in Florida?

Florida does not use a notice of default in the way non-judicial foreclosure states do. In Florida, the lis pendens itself is the triggering public record. It is filed when the lender initiates the foreclosure lawsuit. There is no pre-lis pendens public filing in Florida comparable to the notice of default recorded in states like Texas or Georgia. The lis pendens is the earliest public signal that a borrower is in default and the lender is pursuing legal action.

Should investors target owner-occupied or investor-owned pre-foreclosure properties?

Both produce deals, but the conversations differ. Owner-occupied sellers often need relocation solutions and may have emotional attachment to the property. Investor-owned or absentee-owner properties involve purely financial decisions: the owner compares the offer to the net proceeds after foreclosure. In Florida's high non-resident-ownership market, filtering for absentee owners plus distress signals produces faster, cleaner negotiations.

Sources:

- Florida Statutes, Chapter 702: Foreclosure of Mortgages and Statutory Liens (leg.state.fl.us)

- Florida Constitution, Article X, Section 4: Homestead Exemption (floridabar.org)

- Florida Office of Insurance Regulation: Property Insurance Market Data (floir.com)

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Florida

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card